CRA Mileage Rate 2026: The 73¢ Rate, with One Big Catch

The 2026 CRA mileage rate is 73¢/km for the first 5,000 km, then 67¢. Here's the math, the logbook, and the mistake self-employed drivers make.

CRA Mileage Rate 2026: The 73¢ Rate, with One Big Catch

By Doug

Last updated: May 2026

If you drive for work in Canada, the rate the CRA uses to figure out how much that driving is worth at tax time went up this year. Not by a lot, but a penny a kilometer adds up.

The 2026 CRA mileage rate is 73¢ per kilometer for the first 5,000 business kilometers of the year, and 67¢ per kilometer for every kilometer after that. Drivers in Yukon, the Northwest Territories, and Nunavut get 4¢ extra on each tier.

That's the number you came for. But there's one big catch most people miss, and it changes everything if you're self-employed. We'll get to it.

Five things to know about the 2026 numbers:

- 73¢/km for the first 5,000 business km (provinces). 77¢/km in the territories.

- 67¢/km for every business km after that. 71¢/km in the territories.

- Up 1¢ from 2025 on both tiers.

- Employees only. If you're self-employed, you don't use this rate. You deduct your actual vehicle expenses based on your percentage of business use.

- The CRA wants a logbook with date, destination, purpose, and km on every trip, plus odometer at the start and end of your fiscal year. Keep it for 6 years.

The 2026 rate, the short version

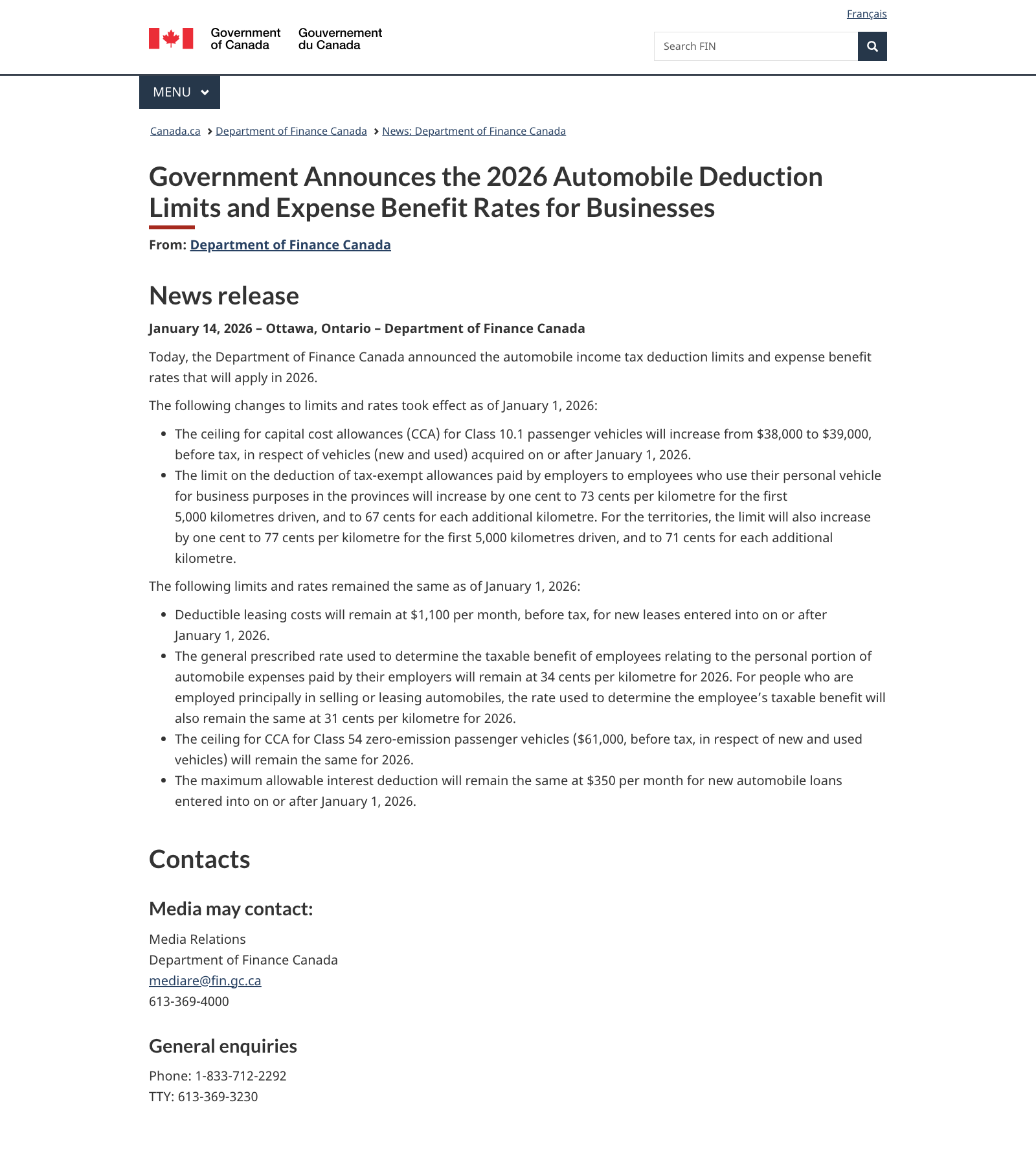

The Department of Finance announced the new 2026 automobile deduction limits and expense benefit rates on January 14, 2026. Here's what changed and what didn't.

| What you're claiming | Provinces | Territories (YT, NWT, NU) |

|---|---|---|

| First 5,000 business km | 73¢/km | 77¢/km |

| Each km after 5,000 | 67¢/km | 71¢/km |

| Operating cost benefit (general) | 34¢/km | 34¢/km |

| Operating cost benefit (auto sales/leasing) | 31¢/km | 31¢/km |

The provincial rates are up one penny from 2025 (last year was 72¢ and 66¢). The territorial premium of 4¢ stays the same.

That penny matters more than it looks. On 12,000 business km a year, it's an extra $120 in your pocket. Over five years, $600. Over a career, real money.

Why the rate changes at 5,000 km

Now, the two-tier thing trips people up. Why does the CRA pay you more for the first 5,000 km than the rest?

The first chunk of kilometers absorbs your fixed costs. Insurance, registration, the part of depreciation that happens just because you owned the car this year. Spread those costs over a small number of kilometers and the per-km cost is high.

After 5,000 km, you've covered most of those fixed costs. What's left is the marginal stuff. Fuel, oil changes, tire wear. So the rate drops.

The threshold is per person, per year. New year, new 5,000-km bucket.

Worked example: 7,000 business kilometers

Say you drove 7,000 business kilometers in 2026 and you're an employee getting reimbursed at the CRA rate by your employer in Ontario.

- First 5,000 km × $0.73 = $3,650

- Next 2,000 km × $0.67 = $1,340

- Total tax-free reimbursement: $4,990

If you were doing the same drive in Whitehorse, the math becomes 5,000 × $0.77 + 2,000 × $0.71 = $5,270. The territorial bump is real money.

That math only works if you 're an employee. Which brings us to the catch.

The catch: employee vs. self-employed

Here's the part that gets missed in nine out of ten articles on this topic.

The 73¢/67¢ rate is the CRA's published ceiling for what an employer can pay an employee tax-free. It's not a flat-rate deduction you can claim if you're self-employed.

If you run your own business (sole proprietor, partnership, single-person corporation paying yourself), you can't multiply your business kilometers by 73¢ and write that off. The CRA wants the actual numbers.

What self-employed Canadians actually deduct

You add up your real vehicle expenses for the year:

- Fuel and oil

- Insurance

- License and registration

- Maintenance and repairs

- Lease payments (subject to the lease cap, see below)

- Loan interest (subject to the cap, see below)

- Capital cost allowance (depreciation, also capped)

- Car washes, parking for business stops (not commuter parking)

Shameless plug: Shoeboxed makes tracking these easy!

Then you multiply that total by the percentage of business use , which is your business km divided by your total km for the year.

If you drove 25,000 km total and 10,000 of those were for business, your business-use percentage is 40%. If your total vehicle expenses for the year were $9,000, your deduction is $3,600.

That's it. The 73¢ never enters the math.

The whole deduction hinges on getting the business-use percentage right. Total km is easy — that's just your odometer at the start and end of the year. Business km is the hard part. It comes from your logbook, every business trip, all year long. If you're not tracking your business kilometers as you drive, you're guessing at tax time, and the CRA reassesses guesses every audit. Track every business trip the day it happens, and the percentage takes care of itself.

What this looks like in practice

Here's a real example from our customer base. I pulled one Eastern Canadian customer's 2026 receipts to see what real-world tracking looks like in the wild.

From January through April, they saved 49 fuel-up receipts: $5,886 in gas, with $647 in HST that's reclaimable as input tax credits if they're GST/HST-registered. Most fills are at the same handful of stations, every receipt is dated and scanned, every one tagged Auto / Fuel. April alone had 37 fill-ups — that's roughly nine a week. This person drives.

Here's what's NOT in those 49 receipts:

- Not one oil change

- Not one tire rotation

- Not one insurance payment

- Not one license or registration receipt

- Not one parking stub for a business stop

If they file T2125 with the actual-cost method using only that $5,886 in fuel, they're leaving real money on the table. Typical Canadian full-coverage auto insurance runs $1,800–$2,400 a year. Maintenance averages $700–$1,000. Add capital cost allowance on the vehicle and any cap-limited lease or loan-interest deductions, and a complete actual-cost claim is often two to three times what fuel alone gets them.

The CRA doesn't care that the receipts are scattered across the glove box, paper bills, and email confirmations. They care that you have them when they ask. The simplest way to not be this customer at tax time: every business-related vehicle expense gets scanned the day you incur it.

The mistake to avoid: Multiplying business km by 73¢ on your T2125. The CRA may catch that, better off just doing it right. Use the actual-expense method, prorated by business-use percentage — and track ALL of the costs, not just fuel.

Employees: when does the rate matter?

If you're an employee and your employer reimburses you at or below the CRA rate per kilometer, the whole reimbursement is tax-free. If they pay you above the rate, the entire allowance becomes a taxable benefit, not just the excess.

If your employer doesn't reimburse you, or pays you a flat allowance that doesn't line up with kilometers driven, you can claim employment expenses instead. That requires Form T2200 signed by your employer, and Form T777 filed with your return.

One thing the CRA doesn't budge on: driving from home to your regular workplace is a commute , not a deductible business trip. It's the same rule whether you're an employee or self-employed.

What records the CRA wants

Whether you use the per-km method (employee) or actual expenses (self-employed), the CRA's expectations on records are the same. They want a logbook.

For each business trip:

- Date of the trip

- Destination (where you went)

- Purpose (why you went there)

- Kilometres driven on that trip

For the vehicle as a whole, you also need:

- Odometer reading on the first day of your fiscal year

- Odometer reading on the last day of your fiscal year

- A new pair of odometer readings any time you swap vehicles mid-year

You keep all of this for six years from the end of the tax year it relates to. The CRA's motor vehicle records page spells out the full requirement.

That sounds like a lot. It is, if you do it by hand. The good news, the CRA also lets you use a shortcut.

Full logbook vs. simplified logbook

The CRA has two paths. Pick the one that fits your patience.

The full logbook

Track every business trip every day. Date, destination, purpose, km. Odometer at the start and end of the year. This is the gold standard, and it's the one the CRA will never argue with.

If you're starting fresh or you don't have a steady driving pattern, the full logbook is the right move.

The simplified logbook (the shortcut)

Once you've kept a full logbook for one complete year (your "base year"), you can use a shortcut in following years. Here's how it works:

- Keep your detailed log for one full base year.

- In a later year, you only need to track a representative three-month period in detail.

- As long as the business-use percentage in your sample period is within ±10 percentage points of the same period in your base year, the CRA will let you scale that sample up to the whole year.

The formula they use:

(Sample year period % ÷ Base year period %) × Base year annual % = Calculated annual business use

That sounds technical. Here's what it looks like with real numbers.

Worked example: simplified logbook

Say in 2024 you kept a full log. Result: you drove 56% for business that year. During the months of April, May, and June 2024, you drove 60% for business.

In 2026, you don't want to track every trip. So you keep a careful log for April through June. That sample comes out to 58% business use.

Plug it in:

(58% ÷ 60%) × 56% = 54.1% business use for 2026.

You apply 54.1% to your total kilometers and to your total vehicle expenses for the whole year. Done.

The 10-percentage-point tolerance is the guardrail. If your sample-period business use comes in at 75% when your base year was 60%, the CRA assumes something material changed and wants you back in a full logbook for that year.

Pro tip, even if you use the simplified method, you still need odometer readings for the start and end of the fiscal year, plus your trip-by-trip log for the three-month sample.

The other 2026 limits that changed

The mileage rate isn't the only number the Department of Finance updated for 2026. If you own or lease a vehicle for business, these matter too.

| Limit | 2025 | 2026 |

|---|---|---|

| CCA ceiling, Class 10.1 (passenger) | $38,000 | $39,000 |

| CCA ceiling, Class 54 (zero-emission) | $61,000 | $61,000 (unchanged) |

| Deductible lease cost cap | $1,100/mo | $1,100/mo (unchanged) |

| Deductible interest cap on auto loans | $350/mo | $350/mo (unchanged) |

The capital cost allowance ceiling for a regular passenger vehicle bumped up $1,000. Everything else held.

Translation: if you bought a $50,000 truck for your business in 2026, you can only depreciate up to $39,000 of it (plus tax). If your monthly lease is $1,400, only $1,100 of that is deductible. If your car loan interest is $500 a month, only $350 of that is deductible.

These caps are why the actual-expense method takes some bookkeeping. You don't get to deduct everything you spend, just what falls under the lid.

How we handle this at Shoeboxed

When I asked our Canadian customers and prospects what they wanted, they told me loud and clear: mileage tracking. So we built it.

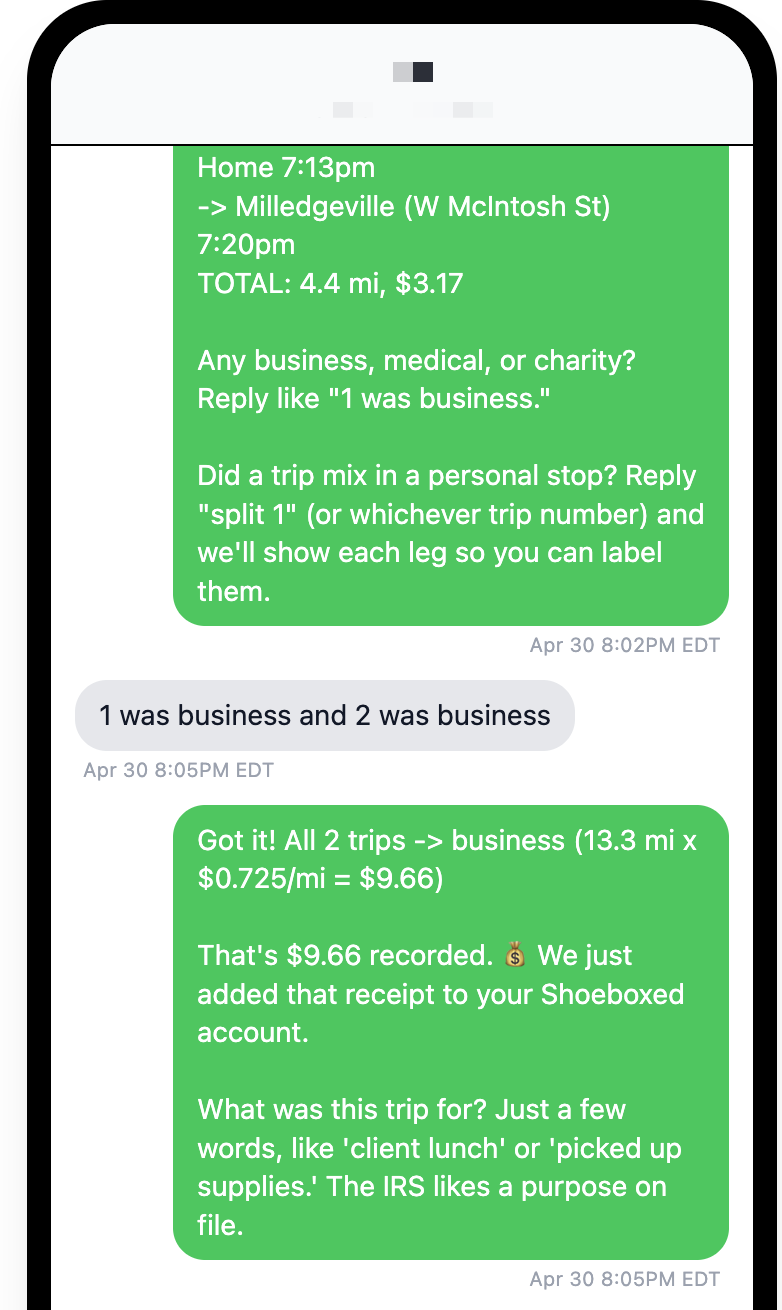

Here's what happens. You turn it on once. We track every trip automatically with GPS — no buttons to press, no app to remember to open, no "did I forget to log that one?" At 8 PM you get one text listing the day's trips: " 3 trips today: Home → Mississauga, Mississauga → Brampton, Brampton → Home. Which were for business?" You reply naturally — " first two were business, lunch with a client" — and we file it.

Heads up: this is from my own US account. Canadian users get the same flow, just km and the CRA rate instead of miles and the IRS rate.

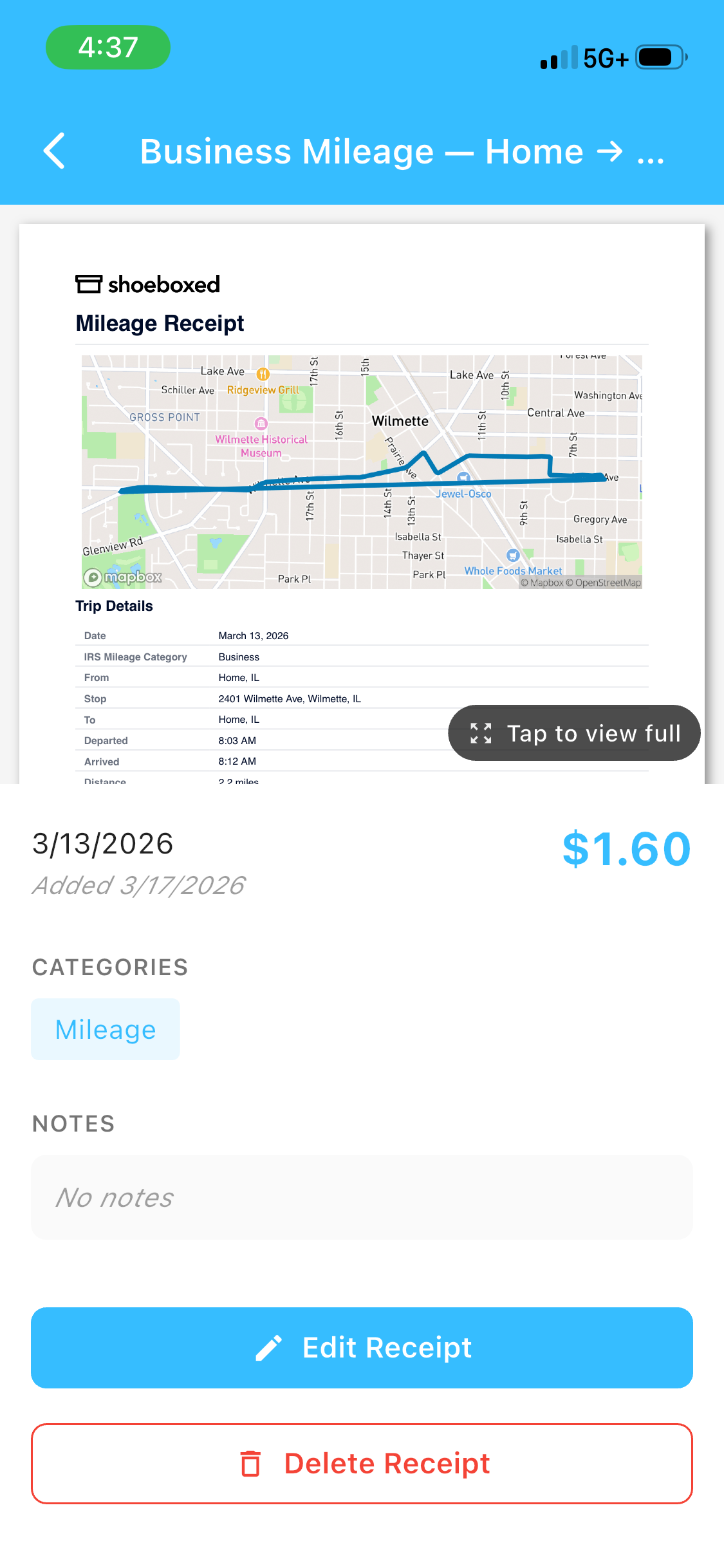

Every business trip becomes a CRA-compliant record with the four fields the agency wants: date, destination, purpose, and kilometers. With a PDF map of the route attached. Saved in your Shoeboxed account forever, sitting alongside your scanned receipts so everything for tax time is in one place.

Also from my US account — the Canadian receipt swaps miles for kilometers and the IRS rate for the CRA rate. Everything else is the same: date, route, deduction, all in your Shoeboxed account.

We apply the right CRA rate automatically — 73¢ for the first 5,000 business km, 67¢ after, with the territorial bump if you're up north — and we keep a running tally so you always know where you are against the 5,000 km threshold. No mental math required.

At tax time your accountant pulls a full year of trip records out of your account in one shot. No retyping. No "I'm sure I drove there in March, what was it for?" No guessing.

That's the pitch. Back to the rate.

FAQ

What is the CRA mileage rate for 2026?

73¢ per kilometer for the first 5,000 business kilometers, then 67¢ per kilometer after that. In Yukon, the Northwest Territories, and Nunavut, the rates are 77¢ and 71¢. These are tax-free allowance ceilings for employer-to-employee reimbursements, set by the Department of Finance on January 14, 2026.

What changed from the 2025 CRA mileage rate?

Both tiers went up by one penny. The 2025 rates were 72¢ for the first 5,000 km and 66¢ after. The territorial premium of 4¢ stayed the same in both years.

Can I use the 73¢ rate as a self-employed deduction?

No. The 73¢/67¢ rate is the CRA's tax-free ceiling for employer-to-employee mileage allowances. If you're self-employed, you deduct your actual vehicle expenses (fuel, insurance, maintenance, depreciation, lease, interest) and multiply that total by your business-use percentage from your logbook. The flat per-km rate doesn't apply.

Why is the rate higher in the territories?

Vehicle costs run higher in Yukon, the Northwest Territories, and Nunavut. Fuel, parts, repairs, and insurance all cost more up north. The 4¢/km premium is the Department of Finance's way of recognizing that.

What about medical mileage in Canada?

The CRA lets you claim travel costs for medical care if you had to drive at least 40 km one way to get treatment unavailable closer to home, and at least 80 km one way to claim things like meals and lodging on top of the kilometers. The simplified per-km rate for medical and moving travel is set by province each year and is published separately from the business mileage rate. Check the CRA's page on eligible medical expenses for the current year's per-province rate.

Do I really need a logbook?

If you want the deduction or the tax-free allowance, yes. The CRA can ask for proof at any point in the six years following the tax year. No logbook, no deduction. A spreadsheet works. A notebook works. An app works. What matters is that you have date, destination, purpose, and kilometers for every business trip, plus odometer readings at the start and end of the fiscal year.

Is the simplified logbook safe to use?

Yes, as long as you've already done one full base year of detailed tracking and your sample-period business-use percentage stays within 10 percentage points of your base year for the same months. If it drifts more than that, the CRA assumes your driving pattern changed and you're back to a full year of detail. The simplified method is the CRA's own published shortcut, not a workaround.

Does my drive to the office count?

No. Driving between home and your regular place of work is a commute, not a business trip. Driving between work and a client site, between two job sites, or to a meeting that isn't your normal office, that counts. This rule is the same for employees and the self-employed.

Sources

- Department of Finance Canada, "Government announces the 2026 automobile deduction limits and expense benefit rates for businesses" (January 14, 2026)

- Canada Revenue Agency, "Motor vehicle records"

Doug runsShoeboxed, the receipt-scanning and mileage-tracking service that's been helping small businesses since 2007 — including hundreds of Canadian customers for over a decade. He bought the company in late 2025.

30 Seconds Could Save You Thousands on Taxes

Self-employed? Get an instant, personalized tax-savings estimate.