Lost a Receipt? Here's What the IRS Needs Instead

Lost a business receipt? The IRS doesn't need paper for any non-lodging lost receipt under $75. Keep a quick log. Download our free template.

Last week you spent $42 at Home Depot on drywall screws for a client remodel. You took an $18 Uber to a client meeting downtown. You ordered a $90 wireless mouse off Amazon.

By Saturday you can't find the Home Depot slip or the Uber email.

Now picture yourself trying to file your taxes. You're staring at a credit-card statement, cursing yourself for losing the tax deductions on the Home Depot screws and the Uber ride because you lost the receipts.

Knowing which kind you lost helps too; the types of receipts guide shows what each one proves and what can stand in for it.

Do you want some good news? You can rest easy, The IRS doesn't need the receipts for under $75. They DO need documentation, but not the actual receipt.

When the IRS needs a receipt, and when it doesn't

Want the short version? Which rule applies depends on the amount. For travel, meals, mileage, gifts, and entertainment under $75, the IRS dropped the paper-receipt requirement years ago. You still keep a short log of what the expense was for, but the receipt itself is optional. The one exception is lodging, where you always save the receipt, no matter the cost.

For the exact IRS language, the lodging exception, and how long to keep everything, see our full guide to IRS receipt requirements and the $75 rule.

The takeaway. Under $75? A quick log entry is all the IRS asks for. Over $75? Keep the receipt if you can, or pair the card statement with the log. The IRS always wants the lodging receipt, regardless of cost.

Why you still need a short log, even when you don't need the receipt

Picture sitting across from an IRS auditor holding your $42 Home Depot slip. The slip shows you spent $42 at Home Depot, but it doesn't show the screws were for a client's basement remodel. Without that piece, the auditor disallows the deduction, and only the log can save it.

For every business expense, the IRS wants five things on record:

- Amount. What you paid.

- Date. When you paid it.

- Vendor. Where you bought it.

- Business purpose. Why this was a business expense.

- Category. Which line of Schedule C it lands on (supplies, office expense, travel, car and truck, etc.).

A receipt covers items 1, 2, and 3, and a card statement covers the same three. Neither one captures items 4 or 5, so the log fills that gap. The IRS isn't picky about the format. They're picky about the five elements.

What if you only have the credit-card statement?

Picture handing your accountant a Chase statement in April with no notes. They flip through it: $80 at Marriott, $45 at Olive Garden, $120 at Home Depot. They look up at you. "What was the Marriott for? Who was at the Olive Garden lunch?" Three months after the fact, you won't remember.

That's the trap: the statement proves you spent the money, but not why. Some owners treat the card statement as proof enough on its own. Others figure it's worthless without the paper. Neither is fully right.

Pub 463 spells the rule out using canceled checks, and the IRS applies the same logic to card and bank statements. Here's the quote:

"A canceled check, together with a bill from the payee, ordinarily establishes the cost. However, a canceled check by itself doesn't prove a business expense without other evidence to show that it was for a business purpose."

The statement proves you spent the money at that vendor, and the log proves the spending was business. Together, that's enough for the IRS.

Don't wait until April and try to guess what you spent all year. Pub 463 says you have to log it close to the event. A weekly entry counts, so a Friday afternoon catch-up for the week works fine. Three months after the fact doesn't.

An old court ruling called the Cohan rule sometimes lets people estimate expenses when records go missing. It won't save you on travel, meals, gifts, or entertainment. The courts hold those categories to stricter substantiation and won't let you guess (see The Tax Adviser for the legal version). For everything else, the IRS frowns on estimating too. Better to keep the log.

The Tax Court has thrown out deductions when taxpayers showed up with card statements but no log kept at the time. Patitz v. Commissioner (T.C. Memo. 2022-99) shows this in action. The court allowed partial deductions for items the taxpayer could document and disallowed the rest.

The Tax Court doesn't accept "I'll piece it together later." The log is what stands between your deductions and the gavel.

The Tax Court doesn't accept "I'll piece it together later." The log is what stands between your deductions and the gavel.

Our free Lost Receipt Substantiation Log (Google Sheets, Excel, PDF)

We built you a log that captures the five IRS-required elements in one row. It's free, no email needed, and comes in three formats so you can pick whichever one fits.

Pick the format that fits: copy the Google Sheet, download the Excel, or print the PDF.

Here's what each column captures, and which IRS element it satisfies.

| Field | What goes here | IRS element |

|---|---|---|

| Date | When the purchase happened | Date |

| Vendor | Store, restaurant, or service name | Vendor |

| City, State | Where the purchase happened | Vendor location |

| Amount | What you paid, tax included | Amount |

| Business Purpose | Why this was business ("drywall for client remodel," "supplies for home office") | Business purpose |

| Category (Schedule C line) | Which Schedule C line this maps to | Category |

| Card Statement Match? (Y/N) | Whether your card or bank statement has a matching line | Audit trail |

The Excel and Google Sheets versions auto-total each Schedule C line for you at year-end. Print the PDF if you prefer to write at the desk by hand.

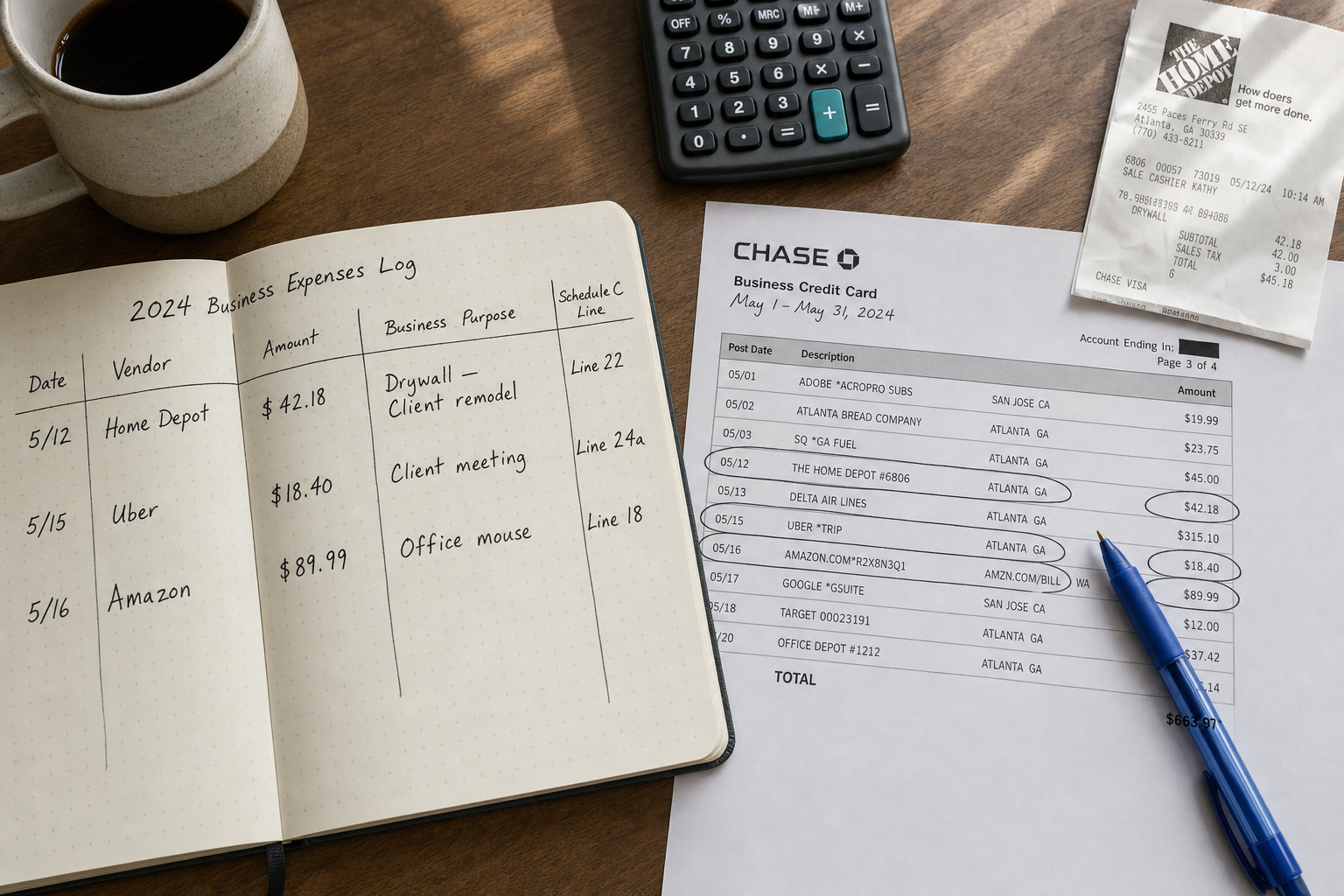

The pair the IRS accepts: a card statement with the lines circled, plus a log filling in the business purpose and the Schedule C line.

The pair the IRS accepts: a card statement with the lines circled, plus a log filling in the business purpose and the Schedule C line.

The handwritten-note pattern works too. Jot the business purpose and category next to the line. Use your check register or your bank app. The IRS calls that a "timely kept record" under Pub 463 ch. 5. It counts as long as you do it close to the time of the purchase.

What 3 million real business receipts tell us about lost paper

Are you curious how often this comes up? We pulled the numbers from our own customer base to find out.

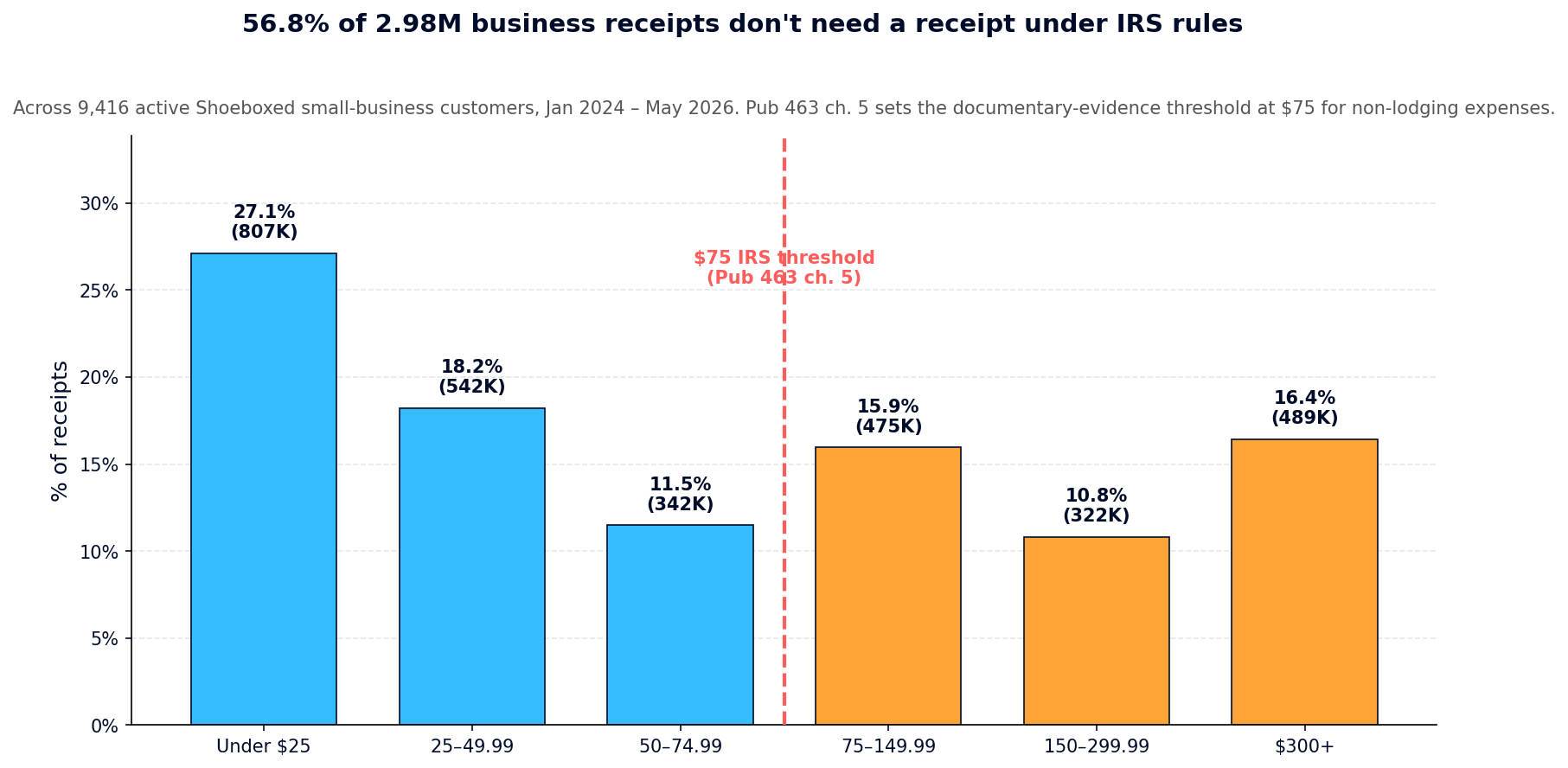

Across 9,416 active Shoeboxed customers since January 2024, we counted 2,977,739 business receipts. 56.8% of them came in under $75. For six in ten receipts our customers track, the IRS asks for nothing more than a short log.

Across 9,416 active Shoeboxed small-business customers and 2.98M receipts since January 2024, 56.8% are under $75.

Across 9,416 active Shoeboxed small-business customers and 2.98M receipts since January 2024, 56.8% are under $75.

Shoeboxed plug: if you track expenses using Shoeboxed, you can download this report quickly and easily.

If we zoom out we see most business expenses run small: more than one in four (27.1%) lands under $25. Big-box stores dominate our customer data, with Home Depot topping the list at 75,000 receipts. Amazon, Walmart, Uber, Costco, Lowe's, Apple, Shell, Target, and McDonald's round out the top ten. The IRS doesn't audit owners over $300 office-supply runs. Real small business owners track $14 lunches, $22 gas fill-ups, and $8 coffees.

For all of those, the IRS accepts a short log entry.

Customers paid for 69.7% of those receipts with a card. That means for most people seven out of ten lost paper receipts have a digital backup sitting in their bank app or card statement. Find the line, pair it with the log, and the deduction holds.

Don't forget your home office and your business mileage

While we're on the topic of paying too much money to the IRS, most Schedule C filers leave two more deductions on the table worth hundreds, or even thousands in deductions. You'll find filing both easier than they sound.

Home office. Picture the corner of your house where the desk lives. The lamp. The laptop. The printer. If you use that space only for business, the IRS lets you deduct part of your rent or mortgage interest, plus utilities, internet, insurance and any other common home expenses. You can use the simplified method, but that only pays $5 per square foot up to 300 sq ft. Use the actual method and you'll likely save a LOT more. To get an instant, personalized estimate, type your address into our home office deduction calculator. It pulls your property data from county records and shows you exactly what deduction waits for you.

Business mileage. Try to remember every client meeting, vendor visit, and supply run you drove to last year and add up the miles. The IRS lets you deduct 72.5 cents per mile (the 2026 rate) for those drives. A Schedule C filer driving 12,000 business miles a year picks up an $8,700 deduction. At a 24% tax bracket, you keep $2,088 in your bank account instead of handing it to the tax man. The IRS wants the same four things on every trip: date, destination, business purpose, miles. The Shoeboxed mobile app auto-tracks every business mile and builds the IRS-compliant log in the background while you drive.

![]()

![]()

How long do you have to keep the receipts and logs?

Good news here too. For most people, the IRS stops looking back three years after you filed the return. They can extend that to six years if you under-reported your income by more than 25 percent. They drop the time limit entirely if they think you committed fraud.

Pub 583 puts it this way:

"You must keep your records as long as they may be needed for the administration of any provision of the Internal Revenue Code."

In plain English, you're safe three years from the day you filed. Scan your receipts, store them digitally, and you'll outlast the IRS by a wide margin.

How to claim the deduction on Schedule C

Wondering which line each receipt goes on? Business expenses go on Part II of Schedule C, spread across the lines that match what you bought. Here's the cheat sheet, pulled straight from the IRS Schedule C instructions.

| What you bought | Schedule C line |

|---|---|

| Online ads, business cards, sponsorships | Line 8 (Advertising) |

| Gas, repairs, mileage on a business vehicle | Line 9 (Car & truck) |

| Subcontractors and 1099 workers | Line 11 (Contract labor) |

| Postage, paper, ink, basic office stuff | Line 18 (Office expense) |

| Rent on a separate office or co-working space | Line 20 (Rent/lease) |

| Tools, supplies, materials | Line 22 (Supplies) |

| State licenses, sales tax | Line 23 (Taxes & licenses) |

| Flights, hotels, business-trip costs | Line 24a (Travel) |

| Business meals (50% deductible) | Line 24b (Meals) |

| Utilities for a separate office | Line 25 (Utilities) |

| Anything else that's ordinary and necessary | Line 27a (Other) |

The Category column on the Substantiation Log maps to these lines one-to-one. Pick the right Schedule C line as you log each expense, and you'll save your accountant half the work before you sit down.

Common questions about lost business receipts

Does the $75 rule apply to credit-card purchases, or only cash?

Both. Pub 463 ties the $75 rule to the dollar amount, not the payment method. A $40 card purchase doesn't need a paper receipt, and neither does a $40 cash purchase. The IRS wants the log either way.

What if I lost a receipt over $75?

Pair the card or bank statement with the log. The statement proves the cost, and the log proves the business purpose. Together, that's enough for the IRS. If you paid cash and there's no card record, call the store. Most big-box retailers will re-print a receipt if you give them the date and your card's last four digits, or a phone number tied to the loyalty program.

Can I reconstruct the log at year-end?

Not per the letter of the law. The IRS doesn't accept a reconstructed-in-April log as a "timely kept record" under Pub 463, and the Tax Court has disallowed deductions on exactly this issue. Catch up weekly if you have to, but don't wait for tax time.

Why is lodging the one exception?

Pub 463 chapter 5 carves out lodging as the single exception. The IRS requires a hotel receipt no matter the cost, even for a $35 motel. Every other non-lodging category gets the $75 threshold.

Is a credit-card statement enough on its own?

Almost never. Pub 463 says a canceled check "by itself doesn't prove a business expense without other evidence." A card statement works the same way. Pair it with the log and you're covered.

Do I need an itemized receipt, or is the card slip enough?

Pub 463 lists four things that count as adequate evidence: amount, date, place, and essential character of the expense. A card slip usually skips the "essential character" piece (what you bought). The log fills that gap.

If what you lost was a store slip, our sales receipt guide shows which facts the replacement needs to carry.

Once you've rebuilt the proof, set up a system so it doesn't happen again. Our guide to storing receipts covers it.

When you don't want to chase paper at all

Picture next April. Your receipts are already scanned, tagged by Schedule C category, and waiting for your accountant. No cupholder dig, no emails to forward, no half-remembered $40 expenses to round down on. That's what Shoeboxed is for.

Forward your receipts to your Shoeboxed inbox, snap a photo, or drop the paper pile in the Magic Envelope. We scan, tag by Schedule C category, and store every receipt as long as the IRS could ask. The Substantiation Log above covers what a scanned receipt can't capture on its own: the business purpose, the category, and the audit trail you'll need if anyone asks.

Use the log on its own if that's all you need. Or let Shoeboxed scan, sort, and store your receipts for you.

Try Shoeboxed risk-free for 30 days →

Can't get the receipt back? You can often still claim the deduction. Here's how to claim deductions without receipts using the Cohan Rule and a simple expense log.

About the author. I'm Doug. I bought Shoeboxed in late 2025 with an SBA loan after fifteen years of running other people's companies as CEO. I'd used Shoeboxed myself back in 2010 at a previous gig and called it magical even then. I use it daily now. Small business owners deserve every dollar they're legally entitled to keep, which is why I bought Shoeboxed and work hard to make it better.

Sources

- IRS Publication 463, Travel, Gift, and Car Expenses.

- IRS Publication 583, Starting a Business and Keeping Records.

- IRS Instructions for Schedule C (Form 1040).

- 26 U.S. Code § 6001, Notice or regulations requiring records.

- 26 CFR § 1.6001-1, Records, in general.

- 26 CFR § 1.274-5, Substantiation requirements.

- IRS Notice 95-50 (1995 amendment raising threshold from $25 to $75).

- IRS Notice 2026-10, 2026 standard mileage rates.

- Patitz v. Commissioner , T.C. Memo. 2022-99

- Cohan v. Commissioner , 39 F.2d 540 (2d Cir. 1930)

30 Seconds Could Save You Thousands on Taxes

Self-employed? Get an instant, personalized tax-savings estimate.