Lost a Restaurant Receipt? Here's What the IRS Actually Accepts

Discover how a restaurant receipt can be a powerful tool for tracking expenses and maximizing tax deductions!

You took a client out to lunch last week. You picked up the check. Now the restaurant receipt is gone. Pocket, cupholder, washing machine, who knows where. It's tax time and you're staring at a credit-card statement wondering if you just lost the deduction on that meal.

Here's the part nobody tells you. If that meal was under $75, the IRS doesn't need that receipt anyway.

When the IRS needs a restaurant receipt, and when it doesn't

There are two cases, and both are simpler than most people think.

Under $75. You don't need a receipt for the meal. The IRS dropped that requirement for small business meals years ago. You still need a short log of what the meal was for, but the receipt itself is optional.

$75 or more. You need documentary evidence. A receipt works, and so does a credit-card or bank statement showing the transaction. The same log applies.

Either way, the piece the IRS cares about is the log. The receipt is the optional part. For the exact IRS language and the full rule, see our guide to IRS receipt requirements and the $75 rule.

A real $12.05 McDonald's receipt from a Shoeboxed customer. Under $75, the IRS doesn't need the paper at all.

A real $12.05 McDonald's receipt from a Shoeboxed customer. Under $75, the IRS doesn't need the paper at all.

Why you still need a short log, even when you don't need the receipt

A receipt only proves you paid the restaurant. It doesn't say why you were there or who was with you, and the IRS needs both of those things to allow the deduction. That's what the log is for.

The Treasury regulation (Treas. Reg. § 1.274-5T(b)(3)) lists five things you have to track for every business meal, no matter the cost:

- Amount. How much you spent.

- Time. The date.

- Place. The restaurant and city.

- Business purpose. Why this meal was business.

- Business relationship. Who was there and how they relate to your business.

A receipt covers items 1 through 3, and a card statement covers the same three. Neither one captures items 4 or 5 on its own, which is why the log is the piece you can't skip.

Once a meal crosses $75, the IRS wants documentary evidence on top of the log. A receipt or a card statement will do.

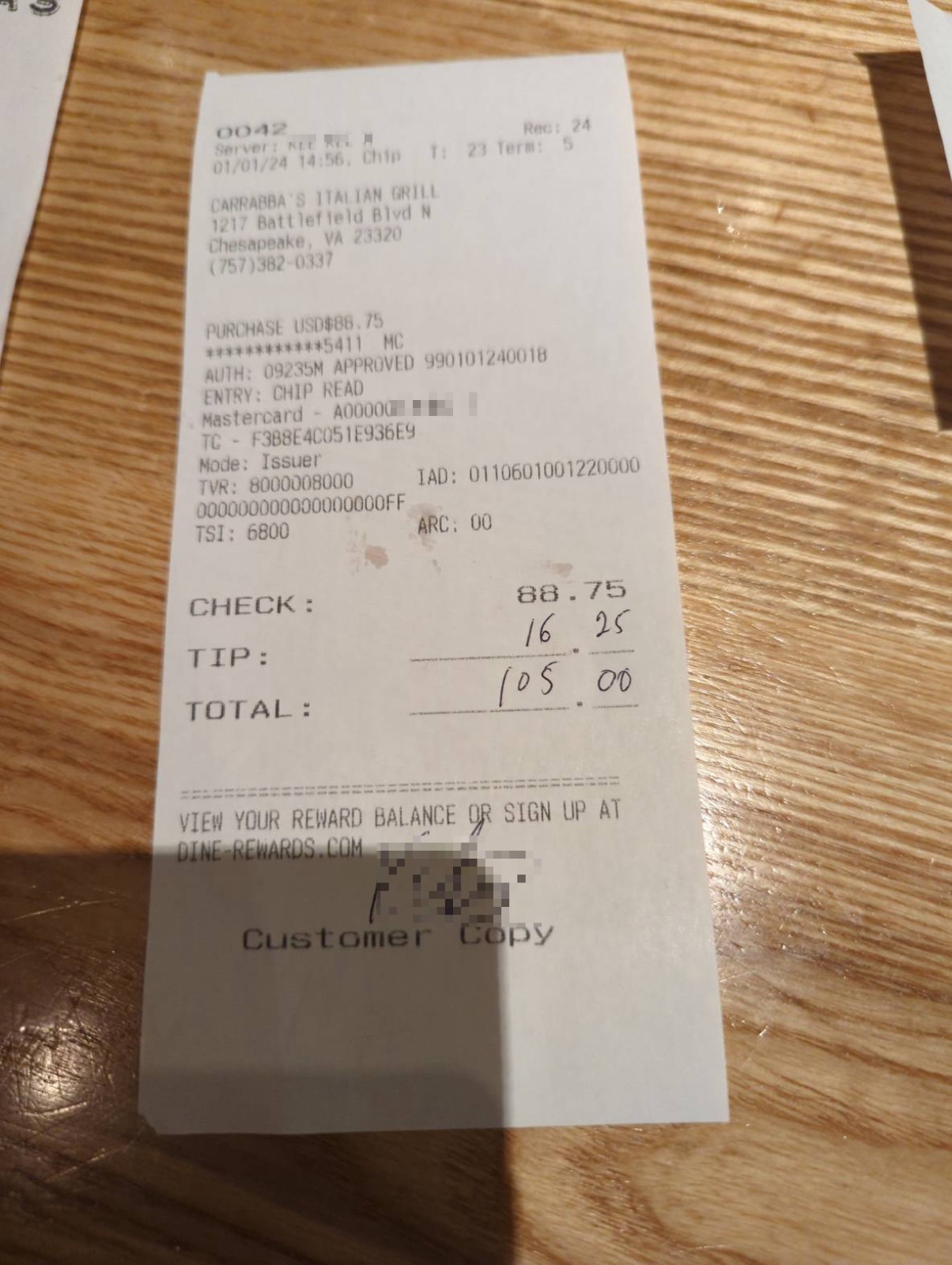

A $105 client dinner. Over $75, the IRS wants documentary evidence alongside your log.

A $105 client dinner. Over $75, the IRS wants documentary evidence alongside your log.

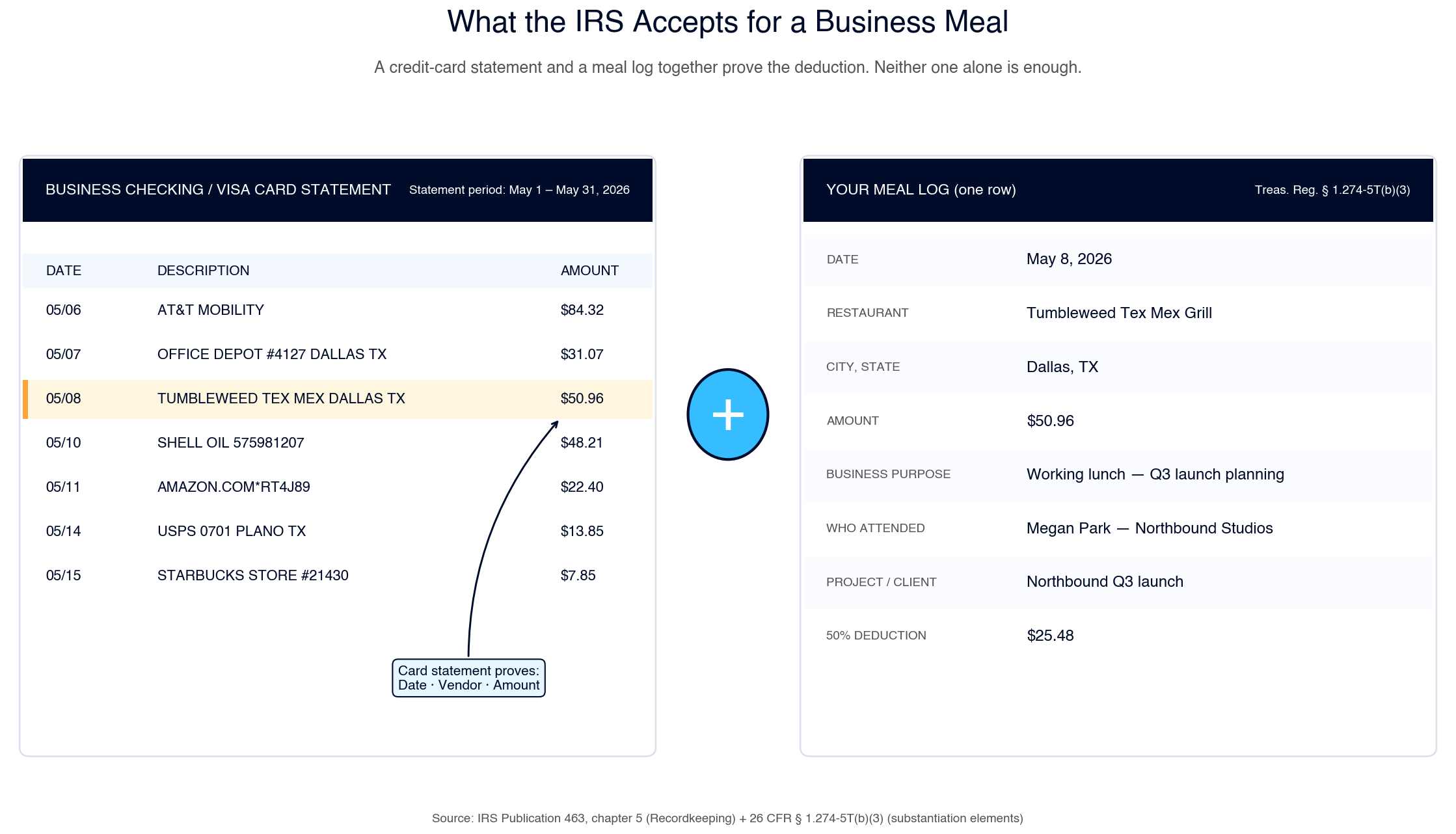

What if you only have the credit-card statement?

Most owners get this wrong in one of two ways: some think a card statement is good enough on its own, while others think it's useless without the paper receipt. Neither belief is right.

Pub 463 talks about canceled checks directly. The same logic applies to credit-card and bank statements:

"A canceled check, together with a bill from the payee, ordinarily establishes the cost. However, a canceled check by itself doesn't prove a business expense without other evidence to show that it was for a business purpose."

The statement proves you spent the money at the restaurant, but it doesn't prove the meal was for business. The log does that part, and together the two of them make you audit-ready.

The pair the IRS accepts: the card statement proves what you paid, the log proves why.

The pair the IRS accepts: the card statement proves what you paid, the log proves why.

The Tax Court has thrown out meal deductions when taxpayers showed up with card statements but no log. A recent example is Patitz v. Commissioner (T.C. Memo. 2022-99), where the court allowed partial deductions for the meals that had records and disallowed the rest.

Don't try to estimate your way out, either. There's an old workaround called the Cohan rule that lets taxpayers ballpark some expenses when records are missing, but it does not save you on meals, travel, or entertainment. As The Tax Adviser puts it:

"the Cohan rule does not apply where specific statutory documentation requirements exist, such as those for travel expenses under Sec. 274(d)."

That means no estimating, and no reconstructing your year in April. The log has to be kept close to the event itself. Pub 463 says a weekly entry counts, so a Friday afternoon catch-up for the week works fine. Three months later does not.

Handwritten tip on the total. This is what most business meal receipts actually look like.

Handwritten tip on the total. This is what most business meal receipts actually look like.

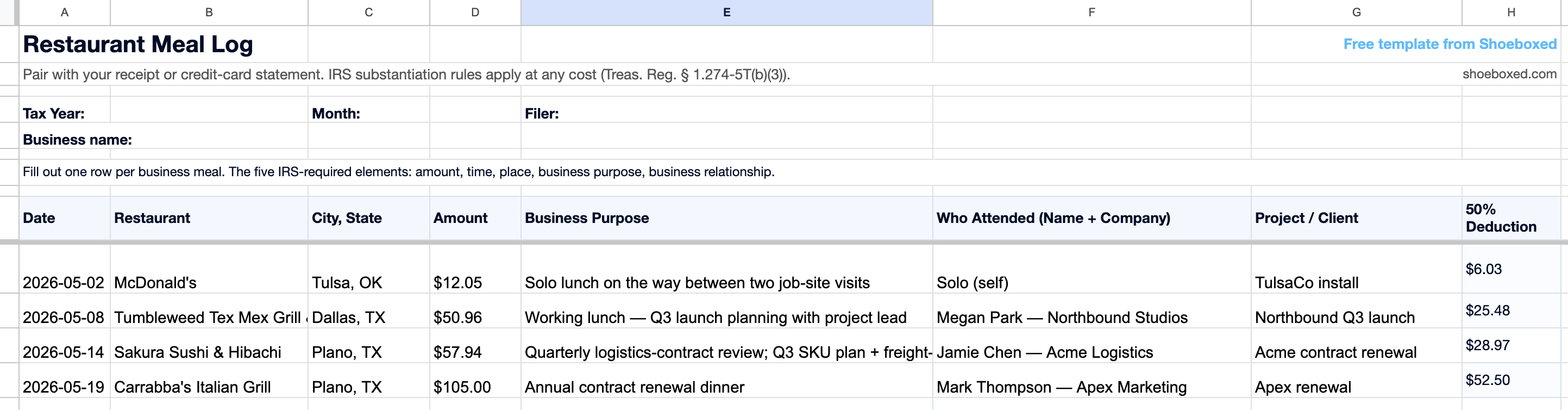

Our free Restaurant Meal Log (Google Sheets, Excel, PDF)

We built a meal log that captures the five IRS-required elements in one row. It's free, no email required, three formats.

Make a copy in Google Sheets · Download Excel (.xlsx) · Print PDF

Field by field, here's what each column captures and which IRS element it satisfies:

| Field | What goes here | IRS element |

|---|---|---|

| Date | When the meal happened | Time |

| Restaurant | Name of the establishment | Place |

| City, State | Where the restaurant is | Place |

| Amount | What you paid, tip included | Amount |

| Business Purpose | Why this was a business expense ("Q3 launch planning," "vendor contract review," "client onboarding") | Business purpose |

| Who Attended | Names and companies of everyone at the meal | Business relationship |

| Project / Client | Internal book-keeping link to the work | (not required by IRS, but your accountant will thank you) |

The Excel and Google Sheets versions do the 50% deduction math for you. They total it at the bottom for Schedule C Line 24b. The PDF is for people who'd rather print it and write at the table.

Run a food truck instead of a dining room? The food truck expense spreadsheet is built from real truck receipts, with a startup-cost worksheet included.

The Restaurant Meal Log with four sample meals. The 50% deduction column auto-totals for Schedule C Line 24b.

The Restaurant Meal Log with four sample meals. The 50% deduction column auto-totals for Schedule C Line 24b.

The handwritten-note pattern works too. Some restaurants give you space on the receipt itself. Jot the business purpose and the attendee right there. That counts as a valid log entry under Pub 463's "timely kept records" rule. The template just makes it cleaner when your accountant or the IRS comes asking.

Pen on the receipt works too. A handwritten note like this counts as a valid log entry.

Pen on the receipt works too. A handwritten note like this counts as a valid log entry.

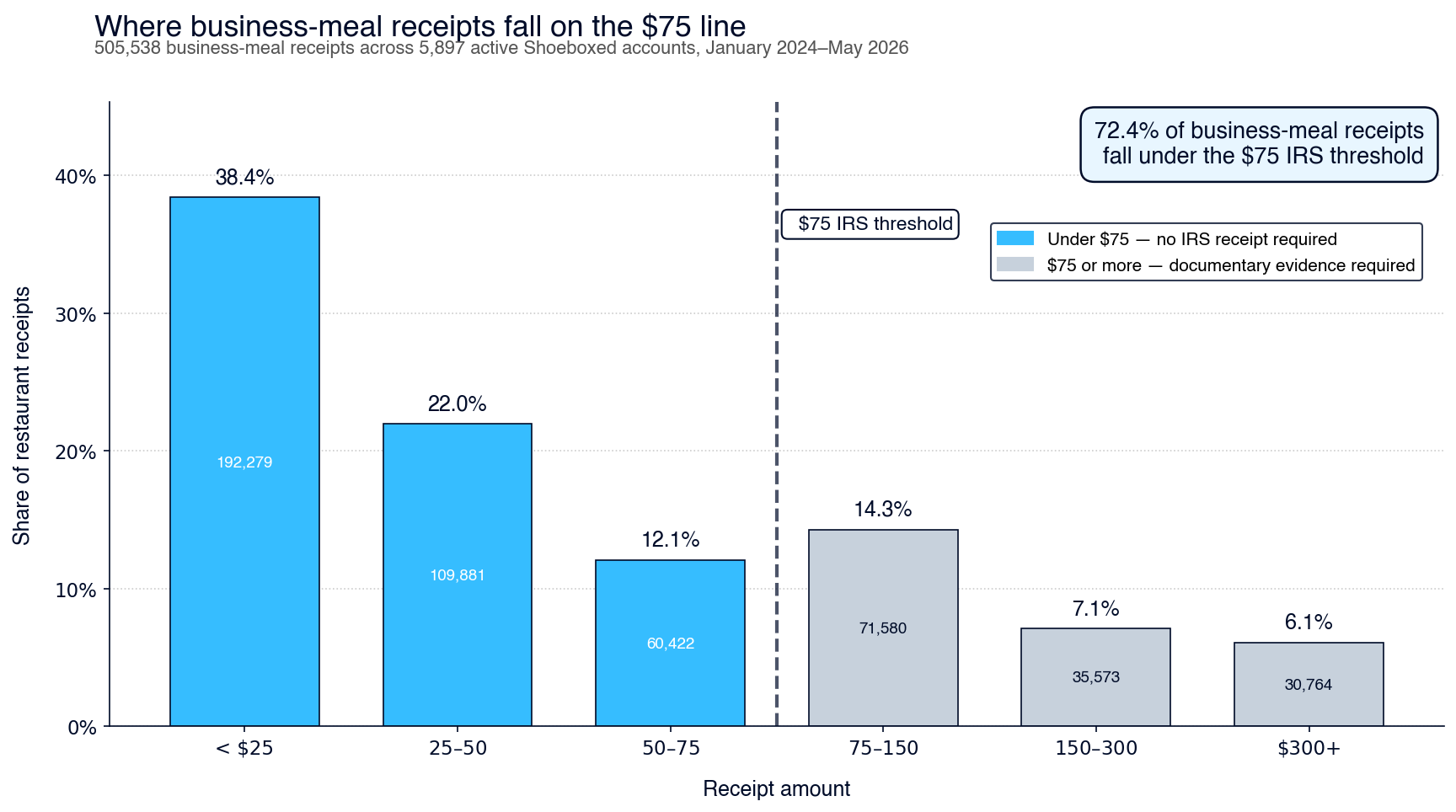

What half a million real receipts tell us about business meals

We looked at 505,538 business-meal receipts across 5,897 active Shoeboxed customers since January 2024.

72.4% of them are under $75.

Nearly three out of four business meals our customers track didn't need a paper receipt at all. A credit-card statement plus a short log was all the IRS asked for.

Across 5,897 active Shoeboxed customers and 505,538 business meal receipts since January 2024, 72.4% are under $75.

Across 5,897 active Shoeboxed customers and 505,538 business meal receipts since January 2024, 72.4% are under $75.

The bigger picture is that most business meals aren't steak dinners. Almost four in ten (38.4%) are under $25. The most-submitted restaurant in our data is McDonald's. The next four are Whole Foods, Chick-fil-A, Starbucks, and Subway. Small-business owners aren't getting audited for $80 client dinners. They're tracking $13 lunches and $8 coffees.

For all of those, a card statement plus a short note is enough.

Don't forget to deduct the drive there

Most people log the meal and forget the drive.

Every time you drive to a business meal, the drive itself is deductible mileage. The 2026 IRS standard rate is 72.5 cents per mile (IRS Notice 2026-10). A 15-mile round trip to a client lunch is $10.88. Drive to 50 business meals in a year and that adds up to $544 in deductions most owners never claim, because they didn't track the drive.

It goes on a different line of Schedule C (Line 9, car and truck expenses). The recordkeeping is the same shape as meals. The IRS wants four things for each trip: date, destination, business purpose, miles driven.

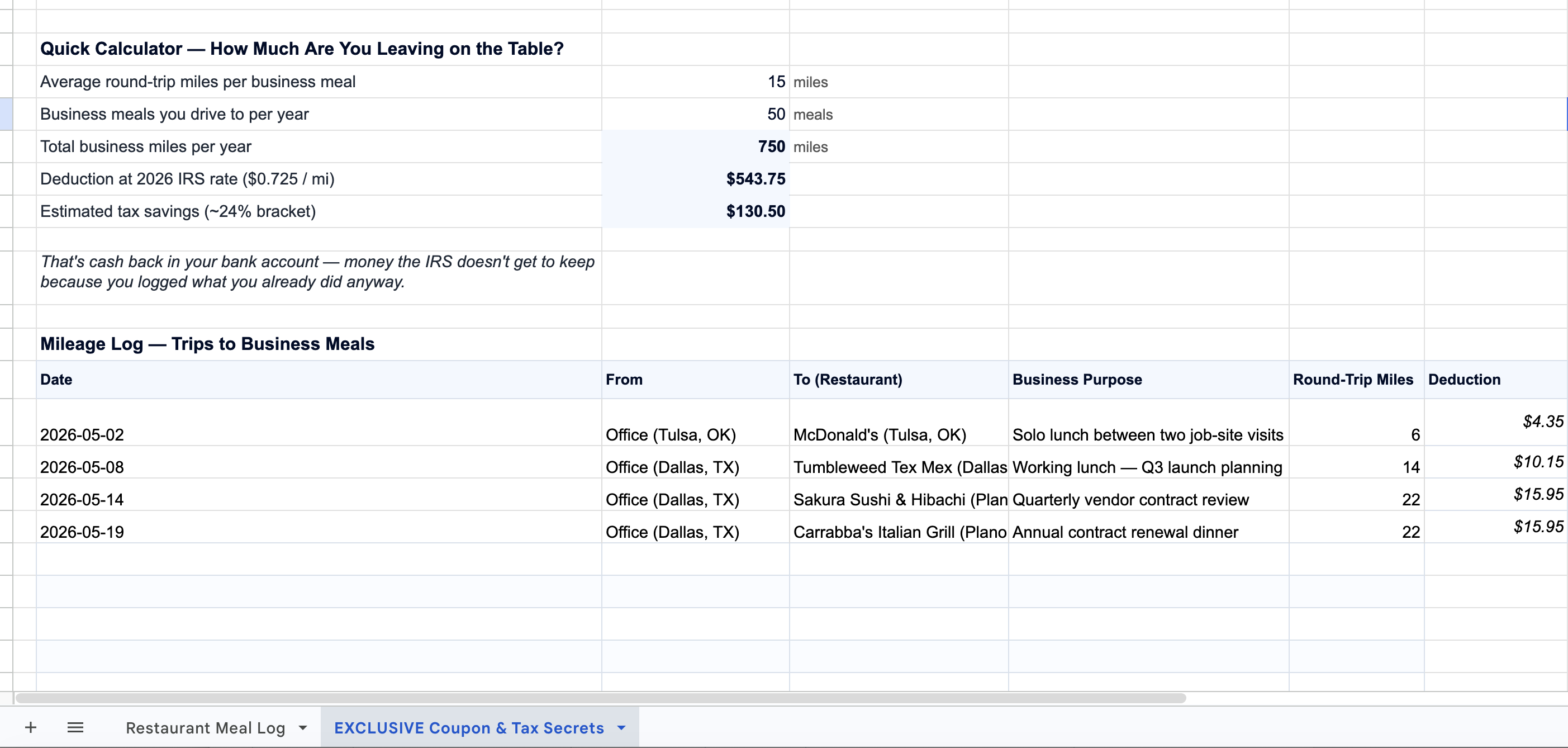

Here's what that looks like for the four sample meals above, with a quick calculator at the top that does the year-end math for you:

Plug your numbers in. Fifty business meals × 15 miles round-trip × $0.725 per mile is $544 in extra deductions most owners never claim.

Plug your numbers in. Fifty business meals × 15 miles round-trip × $0.725 per mile is $544 in extra deductions most owners never claim.

Plug your own numbers into the calculator. A typical Schedule C filer who drives to 50 business meals a year, 15 miles round-trip on average, picks up about $544 in extra deductions. At a 24% tax bracket, that's about $130 in cash that stays in your bank account instead of going to the tax man.

You can either write every trip down at the time or let an app do it for you. The Shoeboxed mobile app auto-tracks every business mile through your phone's GPS and builds the IRS-compliant log in the background while you drive.

How long do you have to keep the receipts and logs?

Three years from the date you filed the return covers most people. The IRS can look back six years if you under-reported your income by more than 25 percent, and there's no time limit at all if they think you committed fraud.

Pub 583 puts it this way:

"You must keep your records as long as they may be needed for the administration of any provision of the Internal Revenue Code."

In plain English, three years from the day you filed the return covers almost everyone. Scan your receipts, store them digitally, and you'll outlast the IRS by a wide margin.

How to claim the deduction on Schedule C, Line 24b

The 50% meal deduction lives on Line 24b of Schedule C. Straight from the IRS Schedule C instructions:

"In most cases, you can deduct only 50% of your business meal expenses, including meals incurred while away from home on business."

The math is simple. Say you spent $4,800 on business meals last year and you've got logs for them. Half is deductible. That's $2,400 off your taxable income. At a 24% tax bracket, you keep about $576 in cash that would have gone to the tax man.

That's per year. Skip the logs and it's per year of missed money.

Common questions about deducting business meals

Can I deduct a single meal I ate alone on a business trip?

Yes, at 50%. A meal you eat while traveling away from home for business is deductible under IRC § 162, with no second party required. Just make sure your log shows the business-trip context.

What about tips?

Tips are part of the meal cost. Add them into the Amount field of the log.

Do I need the itemized receipt, or is the credit-card slip enough?

Pub 463 says a restaurant receipt is enough if it shows the name and location of the restaurant, the number of people served, and the date and amount of the expense. The card slip alone usually skips the "number of people served" part. Pair the card slip with your log and you're covered either way.

Can I expense drinks or beers, alone or with others?

Depends on where you are and who's there.

- With a client, vendor, or business associate. Yes. The drink is part of the business meal. Deductible at 50% as long as the meeting has a real business purpose and your log captures who was there.

- Alone while traveling away from home on business. Yes. The IRS treats meals (drinks included) eaten while traveling for business as deductible at 50%. No second party required. Your log just needs to show the trip context.

- Alone, not traveling. No. Going out for a beer after work in your home city isn't a deductible business meal, even if you spent the whole drink thinking about work.

- One limit to know about. Section 274(k) of the tax code blocks the deduction if the meal is "lavish or extravagant under the circumstances." A $400 bottle of wine over a quick lunch with a client is the kind of line item that gets flagged.

- Entertainment is out. Since the 2017 Tax Cuts and Jobs Act, sports tickets, concerts, and club covers are not deductible, even with a client at the table. Food and drinks consumed at the entertainment are deductible only if separately invoiced from the entertainment.

How Shoeboxed handles all of this for you

Most Schedule C filers don't have a system. They dig through emails and pockets in April, find half of what they need, and round down rather than ask their accountant to chase it.

April is the wrong time to discover the log was missing.

Shoeboxed exists for exactly this. Forward your restaurant receipts to your Shoeboxed inbox, snap a photo with the app, or drop them in the Magic Envelope. However they show up, we scan them, tag them as Meals & Entertainment, and store them for as long as the IRS could ask. The meal log above fills in what a scanned receipt can't capture. The business purpose. The people across the table.

Use the log on its own if that's all you need. Use Shoeboxed if you want the whole receipt-management piece handled.

Try Shoeboxed risk-free for 30 days →

Sources

- IRS Publication 463, Travel, Gift, and Car Expenses — irs.gov/publications/p463

- IRS Publication 583, Starting a Business and Keeping Records — irs.gov/publications/p583

- IRS Instructions for Schedule C (Form 1040) — irs.gov/instructions/i1040sc

- 26 U.S. Code § 274 — Disallowance of certain entertainment, etc., expenses — law.cornell.edu/uscode/text/26/274

- 26 CFR § 1.274-5 — Substantiation requirements — law.cornell.edu/cfr/text/26/1.274-5

- 26 CFR § 1.274-5T — Substantiation requirements (temporary) — law.cornell.edu/cfr/text/26/1.274-5T

- IRS Notice 2026-10 — 2026 standard mileage rates (IRS announcement)

- Patitz v. Commissioner , T.C. Memo. 2022-99

- Cohan v. Commissioner , 39 F.2d 540 (2d Cir. 1930)

30 Seconds Could Save You Thousands on Taxes

Self-employed? Get an instant, personalized tax-savings estimate.