Transaction Receipt: What It Is + Where to Find the Transaction Number

A transaction receipt is your proof that a payment went through. See a real example with the transaction number labeled, learn how it differs from the receipt number, and find out how long to keep yours.

Updated June 2026.

A transaction receipt is the slip, email, or PDF you get when a payment goes through. It shows what you bought, the date, the amount, how you paid, and a transaction number that ties it all back to that one payment.

It does not matter if the receipt is paper or digital. Both prove the money moved.

If you came here hunting for the transaction number on a receipt you are holding, scroll down to the labeled example. I marked it for you, in orange.

I am Doug. I own Shoeboxed, and since 2007 we have scanned over 57 million receipts for more than 552,000 small businesses. I have looked at more transaction receipts than any sane person should. Let me walk you through what is on one, where the numbers hide, and which parts matter when money or taxes are on the line.

What a transaction receipt is

Every time a register, card reader, or website takes your payment, the system records the sale and prints or emails you the proof. That proof is the transaction receipt. The name sounds formal, but it is the receipt you already get every day. The paper slip from the hardware store counts. So does the email from an online order, and the PDF your software vendor sends each month.

A typical card transaction receipt. The store, the items, the math, and the payment details all live on one slip. (Cedar & Pine Hardware is made up for the example.)

A typical card transaction receipt. The store, the items, the math, and the payment details all live on one slip. (Cedar & Pine Hardware is made up for the example.)

A transaction receipt does two jobs at once. For the customer, it is proof of purchase, the thing that gets you a return, an exchange, or a warranty claim. For the business, it is a record of income and, on the buying side, the document that backs up a deduction at tax time.

You will hear cousins of the term, like purchase receipt, sales receipt, e-receipt, or payment receipt. They all describe the same basic document, just named for how or when you got it. If a payment happened and you got a record of it, that record is a transaction receipt.

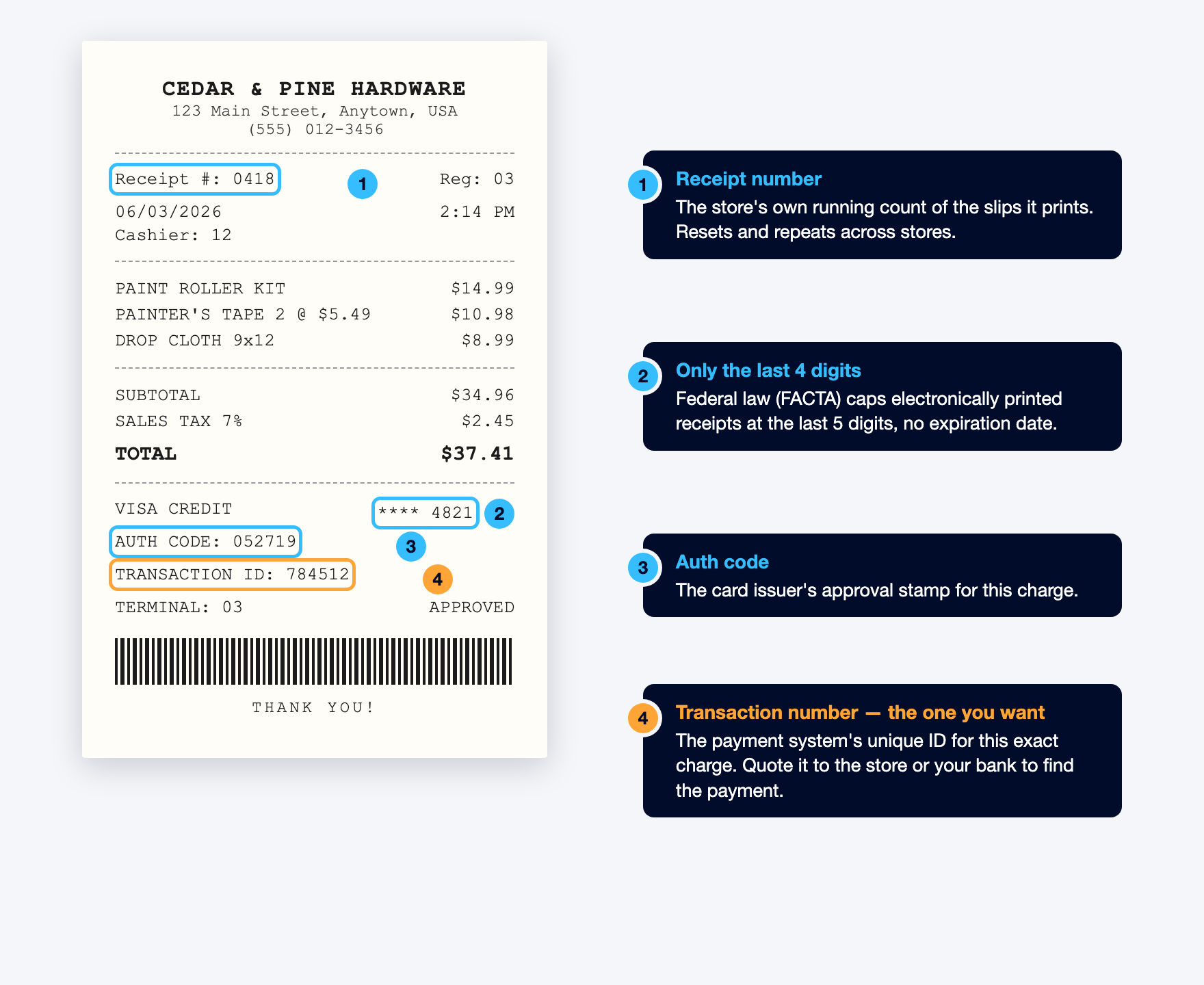

Where the transaction number is on a receipt

On most printed receipts, the transaction number sits near the bottom, in the block of codes by the payment details.

- Check the payment block at the bottom first, near the card type and the word APPROVED.

- Look for a label like "Transaction ID," "Trans #," or "Ref #."

- No luck there? Some stores print it near the top, next to the register and cashier numbers.

- On email receipts, look under the order summary at the bottom of the message.

Here is a real layout with everything labeled.

Where the numbers live on a card transaction receipt. The transaction number, labeled in orange, is the one that identifies this exact payment. (Cedar & Pine Hardware is made up for the example.)

Where the numbers live on a card transaction receipt. The transaction number, labeled in orange, is the one that identifies this exact payment. (Cedar & Pine Hardware is made up for the example.)

The transaction number is the unique ID the payment system stamps on that one charge. No other payment shares it, which makes it the magic word when something goes wrong. Quote it to the store and they can pull up your sale in seconds. Quote it to your bank and they can trace the charge during a dispute or a refund that never landed.

Before you call anyone about a charge, find that number. It saves you from digging through dates, register numbers, and amounts, because the store can find your payment from that one number.

Receipt number vs. transaction number: not the same thing

People mix these two up, and I get why: both are numbers printed near each other on the same slip. Here is the difference.

The receipt number is the store's own running count of the slips it prints. Receipt #0418 means this register has printed 418 receipts, and tomorrow some other store in town will also print a #0418. The transaction number comes from the payment system, and it is unique to that single charge across the whole network that processed it.

| Receipt number | Transaction number

---|---|---

Who assigns it | The store's register or point-of-sale system | The payment processor or card network

What it counts | Slips printed at that store, in order | One unique payment, never repeated

When you quote it | Returns and exchanges at that store | Card disputes, missing refunds, bank questions

You may also spot an auth code on card receipts. That is the card issuer's approval stamp for the charge. It is a separate number with a separate job. For everyday life, remember one rule: the store cares about the receipt number, the bank cares about the transaction number.

What's on a transaction receipt

Ignore the logo and the barcode, and every dependable receipt carries the same handful of fields. You get the business name and location, the date and time, what was sold, the amount with tax, and how it was paid. That list is not an accident. It lines up with the test the IRS uses for receipts, straight from Publication 463:

"Documentary evidence will ordinarily be considered adequate if it shows the amount, date, place, and essential character of the expense."

IRS, Publication 463

That means the amount, the date, the place, and what it was. If your receipt shows those four, it does its job with the IRS, whether it came off a thermal printer or out of your inbox. The transaction number is a bonus. The IRS does not require it, but it is what lets a person find the payment again later.

Is a transaction receipt proof of payment?

Yes. A transaction receipt only exists because a payment cleared, so it is proof of payment by definition. The register prints it after the card reads APPROVED, not before.

People also ask whether a payment receipt is a separate thing from a transaction receipt. For a small business, no. "Payment receipt" frames it from the seller's side, a note that money came in, and "transaction receipt" frames it from the payment's side. Same slip, same fields, same job.

The one case where wording matters: an order confirmation is not a receipt. A confirmation says "we got your order." A receipt says "we got your money." If a seller charges you at shipping time, the receipt shows up when the charge does.

How to get a transaction receipt

You have three reliable paths.

First, at the point of sale: registers and card readers print one automatically, and online checkouts email one. If you are about to walk away without it, ask, because reprinting on the spot beats every other option.

Second, ask the merchant. Call the store, say you need a copy of a receipt, and give them the transaction number, the card's last four digits, or the date and amount. Big retailers can often look up your purchase from the card itself.

Third, check your bank or card statement. The statement line is not a full receipt, but it carries the date, amount, and a reference number, which is enough to ask the merchant for the real thing. If the receipt is gone for good, here is what to do about a lost receipt. Receipts from a bank or an ATM work differently, and we cover those in our guide to bank transaction receipts.

There is a fourth path, and it is the one I would pick: keep your own copy automatically, so you never have to ask anyone. That is the problem Shoeboxed was built to solve. Send us a receipt and we store the actual image, and our software pulls out the vendor, the date, and the total, the key fields the IRS wants to see.

Getting receipts in is the easy part. Pick whichever way fits the receipt in your hand:

- Snap a picture in the app.

- Forward the email to your Shoeboxed address.

- Let our Gmail plugin pick them up on its own.

- Upload or drag and drop on the website.

- Drop the paper in a prepaid Magic Envelope and mail it to us.

We keep everything for as long as you have an account, so the receipt from three years ago is one search away.

Why your receipt only shows the last digits of your card

Look at the card line on any printed receipt and you will see something like **** 4821. The store is not hiding anything from you, it is following federal law. A rule called FACTA caps what stores may print:

"...no person that accepts credit cards or debit cards for the transaction of business shall print more than the last 5 digits of the card number or the expiration date upon any receipt provided to the cardholder at the point of the sale or transaction."

Fair and Accurate Credit Transactions Act (FACTA), 15 U.S.C. § 1681c(g)

The rule covers electronically printed receipts, which means most of what registers spit out today. Handwritten receipts and old-style card imprints are exempt, which is one more reason the carbon-copy receipt book in your drawer should never carry a full card number.

The upshot is good news. A printed receipt is safe to keep, hand to your bookkeeper, or photograph, because nobody can charge anything with the card number on it.

How long to keep transaction receipts

Keep any receipt tied to your business, a rule the IRS spells out in Publication 583:

"You should keep supporting documents that show the amounts and sources of your gross receipts."

IRS, Publication 583

The number of years depends on your situation. Here is how far back the IRS can look:

| Your situation | Keep records for |

|---|---|

| A normal tax return | 3 years |

| You left off more than 25% of your income | 6 years |

| You claimed a loss for a bad debt or worthless stock | 7 years |

My rule for most small businesses: keep everything seven years and never think about it again. The catch is the paper itself. Thermal receipts fade, and a faded receipt proves nothing. For the full picture of what the IRS expects a receipt to show, here are the IRS receipt requirements.

If you're hanging on to paper for now, our guide on how to keep receipts from fading covers how to slow it down before the proof disappears.

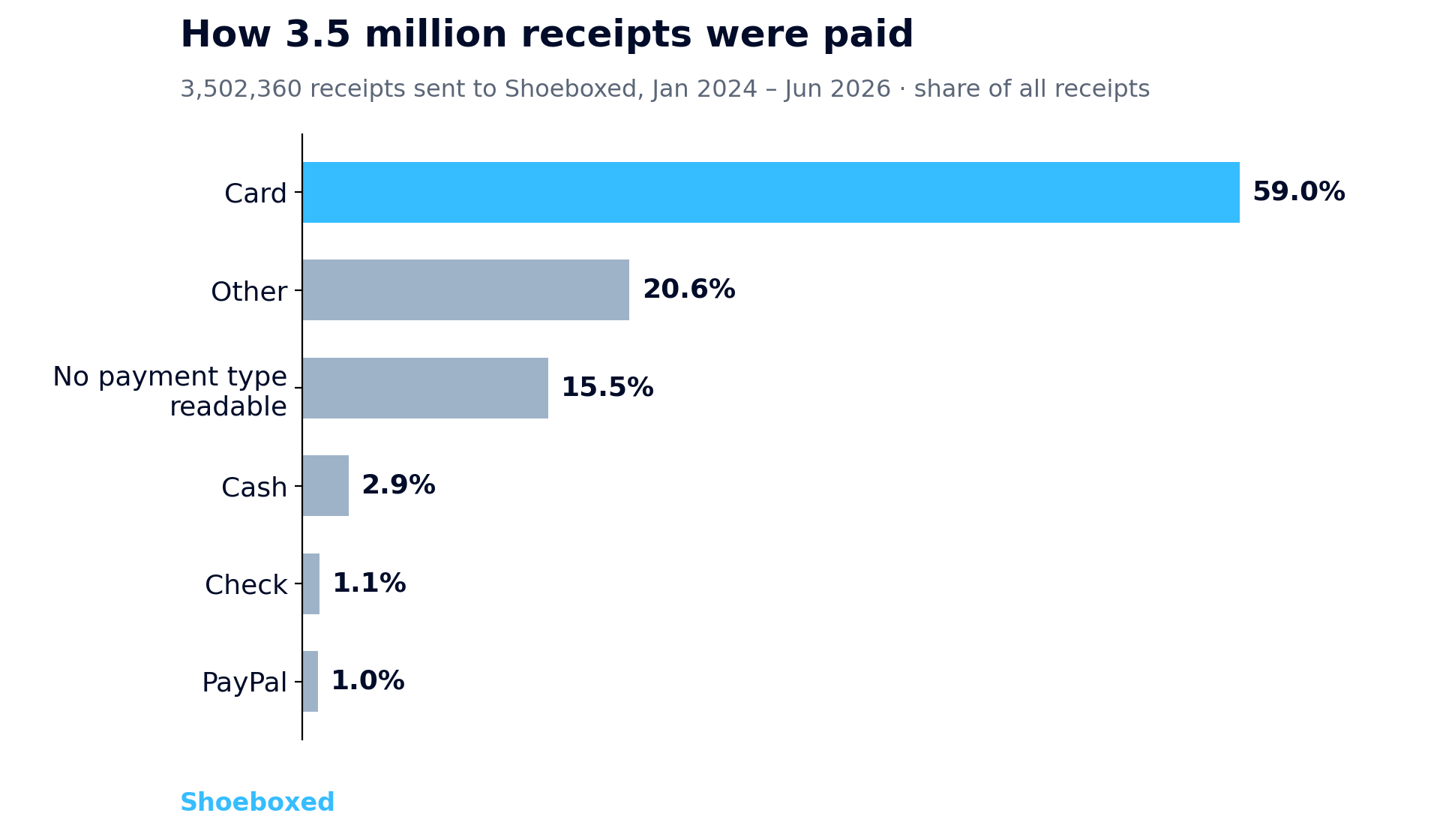

What 3.5 million receipts tell us about transaction receipts

Since January 2024, customers have sent us 3,502,360 receipts to scan and organize. We track how each one was paid, and the mix says a lot about what lands in a small business's pile.

How 3,502,360 receipts sent to Shoeboxed since January 2024 were paid. Shares are of all receipts in the period.

How 3,502,360 receipts sent to Shoeboxed since January 2024 were paid. Shares are of all receipts in the period.

59% arrived paid by card. Those are card transaction receipts, the same kind as the labeled example above. Cash came in at 2.9% and checks at 1.1%, which means card slips outnumber cash receipts twenty to one in a typical pile.

The number that should make you wince is the 15.5% that arrive with no readable payment type. Those are the faded, cropped, and crumpled ones. The bottom of the slip fades first, and that is where the payment details and the transaction number sit. The most useful numbers on the receipt live in its most fragile spot.

Keep every transaction receipt without the shoebox

The hard part of transaction receipts is not getting them. Registers hand them to you all day long. The hard part is keeping them readable and easy to find years later, when your accountant or the IRS asks.

That is the job Shoeboxed does. Every receipt you send in becomes two things. We keep the image itself, and we build a clean record with the vendor, date, total, tax, and payment type, filed into a category. The app, the email forward, the Gmail plugin, and the Magic Envelope all feed the same account.

The records stay in your account for as long as you have one, and even if you ever leave, you can download everything. The paper can fade all it wants, because the record is safe.

Never lose a receipt again. Join over a million businesses that scan receipts, sort them into categories, and build IRS-ready expense reports with Shoeboxed. See how it works.

And if you run your business from home, our free home office deduction calculator estimates what your home office is worth on your taxes from your address. The same habit that saves your receipts is the one that finds money like that.

For the bigger system, here is our guide to receipt organization and management.

For the storage side, our receipt storage guide shows how to set up one home for every slip.

Frequently asked questions about transaction receipts

Where is the transaction number on a receipt?

Usually near the bottom, in the payment block, labeled "Transaction ID," "Trans #," or "Ref #," close to the card type and auth code. Some stores print it near the top with the register number, and email receipts put it under the order summary.

Is a transaction receipt proof of payment?

Yes. It prints only after the payment clears, so it proves the money moved. For a dispute, pair it with the transaction number so your bank can trace the exact charge.

What is the difference between a payment receipt and a transaction receipt?

For practical purposes, nothing. Both name the same document: the record a payment produces. The thing to watch for is an order confirmation, which confirms the order but not the payment.

What are the 4 types of receipts?

Most lists break receipts into sales receipts, cash receipts, e-receipts, and gross receipts, though the categories vary by who is counting. We cover each one in our guide to the types of receipts.

How do I get a copy of a transaction receipt?

Ask the merchant. With the transaction number, the card's last four digits, or the date and amount, most can re-pull it. Your card statement carries enough detail to start that conversation. And if you keep your receipts in Shoeboxed, search for the vendor or the date and download the copy yourself.

Is the transaction number the same as the order number?

No. The order number tracks your purchase through the seller's system, and the transaction number tracks the payment through the card network. A single order can even produce more than one transaction number if it ships, and charges, in pieces.

Final thoughts

A transaction receipt is a simple thing. One slip of paper or one email proves one payment. Know where the transaction number sits and keep the slip readable. That will make a dispute, a missing refund, or an audit letter much easier to get through.

The paper will not take care of itself, and that is the part we handle. Scan your receipts, file them, and the records will outlast the ink.

About the author. I'm Doug. I bought Shoeboxed in late 2025 with an SBA loan after fifteen years of running other people's companies as CEO. I'd used Shoeboxed myself back in 2010 at a previous gig and called it magical even then. I use it daily now. Small business owners deserve every dollar they're legally entitled to keep, which is why I bought Shoeboxed and work hard to make it better.

Sources

- IRS, Publication 463, on what counts as adequate proof of an expense: the amount, date, place, and essential character.

- IRS, Publication 583, on keeping documents that show your gross receipts.

- IRS, How long should I keep records, on the 3, 6, and 7 year windows.

- Cornell Law School LII, 15 U.S.C. § 1681c(g), the FACTA card-number truncation rule.

30 Seconds Could Save You Thousands on Taxes

Self-employed? Get an instant, personalized tax-savings estimate.